The Tariff Pass-Through Decision: A C-Suite Framework for 2026

Tariffs are back as a P&L variable. The C-suite framework for deciding what to pass through, what to absorb, and where to use pricing to defend margin - without a price-elasticity model.

The Federal Reserve's view of tariff pass-through has shifted decisively. Dallas Fed research published in May now describes a "full pass-through" — companies, on average, transferring tariff costs to consumers rather than absorbing them. The Cavallo team at Harvard, working from micro-level retail price data, puts the retail leg of tariff pass-through at roughly 20 percent so far, with the rest sitting upstream at manufacturers and wholesalers. Core inflation in March 2026 came in at 3.2 percent. The Fed's own counterfactual says it would have been 2.3 percent without the tariff wave.

Translation for anyone running pricing: the easy phase is over. The pre-tariff inventory cushion is gone, supplier cost notices are arriving on a weekly cadence, and the question your board will ask you at the next earnings call is not whether to pass tariffs through — it is how much, on what, and how visibly.

This piece is about the decision frame that question deserves. "Pass it through" is the wrong unit of analysis. Tariff pass-through is a portfolio of decisions, each tied to a specific SKU tier, a specific competitor reference, and a specific consumer signal. Mid-market retailers who run that portfolio with discipline hold margin. Retailers who treat it as a single CFO meeting give up two to three points of operating margin without realising it.

The macro has shifted from "absorb" to "transfer"

For most of 2025, the dominant retailer response was absorption. That made sense at the time. Inventory had been front-loaded ahead of the schedule, the consumer was still adjusting to post-pandemic price levels, and the competitive risk of being the first to raise prices outweighed the margin pain of holding the line. Whirlpool's roughly $300 million tariff absorption and 220-basis-point margin hit was the visible face of that period. Levi Strauss has guided to a 150-basis-point tariff headwind in 2026 even after pricing actions.

That posture is breaking. Three things have changed at the same time.

First, the pre-tariff inventory is materially drawn down. Goods sold today were imported under the new schedule, not the old one. The accounting cushion that let retailers report "tariff impact minimal this quarter" has thinned to almost nothing.

Second, the consumer has re-anchored. Cavallo's data shows imported goods rose roughly twice as much as domestic ones following the 2025 tariff measures, and cheaper varieties saw the biggest increases — roughly 5 percent versus about half that for premium SKUs between October 2024 and September 2025. Shoppers expect higher prices in tariff-exposed categories. The window for being the price leader on the way up is open.

Third, the cost notices have become continuous. Suppliers no longer issue a single annual line. Mid-market retailers now receive multiple cost-adjustment letters per quarter on overlapping tariff schedules. Pricing teams that batch those into a quarterly review fall behind the underlying cost curve.

Put together, the question has changed shape. It is no longer whether to pass tariffs through. It is how to run a continuous, structured pass-through that protects key value items, recovers margin on the long tail, and gives the consumer a story they can read.

Three traps the "pass it through" frame creates

Most of the margin damage we see in mid-market retail right now comes from one of three sequencing mistakes. Each is a symptom of treating pass-through as a single decision instead of a portfolio.

Trap one: treating the catalog as one decision. Tariff exposure is highly uneven. A 30,000-SKU catalog might have meaningful tariff content in 6,000 of those SKUs and essentially none in the rest. Within the exposed group, the right pass-through rate differs by an order of magnitude — close to zero on the top-100 key value items where the competitive reference is sharp, much closer to full pass-through on the long tail where reference pricing is weak and substitution risk is low. Retailers who set a single corporate pass-through percentage (the dreaded "let's do 60 percent") end up overpricing the items the consumer notices and underpricing the items nobody is checking. The headline number looks reasonable. The basket experience and the recovered margin both fall short.

Trap two: confusing absorption with strategy. "We're absorbing the tariff" sounds like a strategic stance, but in most pricing organisations it is the absence of one. Real absorption is bounded — a specific list of items, for a specific duration, with a specific competitive purpose, and a recovery path defined elsewhere in the catalog. Unbounded absorption is a margin leak with a press release attached. The C-suite test is simple: if your finance team cannot tell you which SKUs are being deliberately absorbed and how that cost is being recovered on adjacent items, you do not have a pass-through strategy. You have a postponement.

Trap three: mistaking lag for forgiveness. The seven-month lag between landed-cost increases and retail price changes that the academic literature now documents is a physical lag — inventory turn, replenishment cycles, contractual price-protection windows. It is not a strategic option. Retailers who interpret the lag as "we have seven months before we need to act" are choosing to take the cost hit on the back side. The retailers who hold margin are deciding weekly which lots of incoming cost to pass through, which to defer, and which to neutralise through assortment — at the same cadence the cost notices arrive.

The three-tier pass-through decision

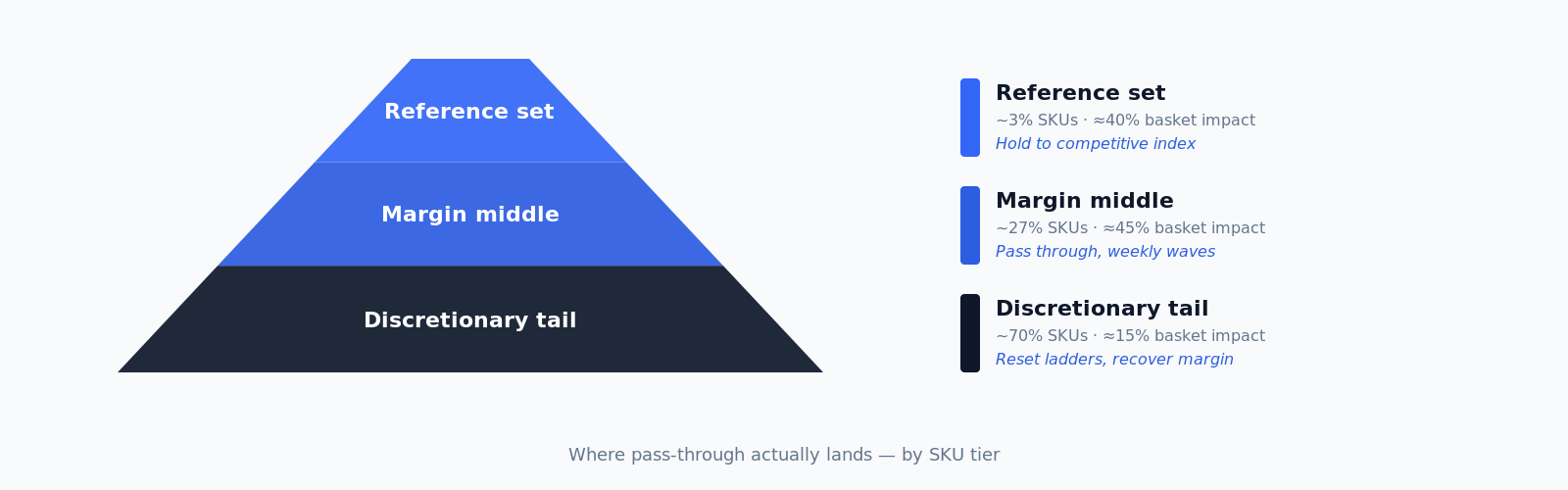

A useful frame for the boardroom is to stop thinking about pass-through as a single percentage and start thinking about it as three different decisions on three different parts of the assortment.

The first tier is the competitive reference set — the items where the consumer or a competitor's shelf is the binding price constraint. These are key value items, traffic drivers, and items that anchor basket perception. Pass-through here is bounded by what the competitive set does, not by the supplier's cost letter. The right rule is usually a relative one: stay within a defined index of the reference set, and if the reference set moves, move with it. If the reference set does not move, hold. Margin recovery on these items, if it happens at all, comes from supplier negotiation, pack-size adjustment, or assortment swap — not from a unilateral price increase.

The second tier is the margin-sensitive middle — items with real volume but weak external reference pricing. This is where the bulk of recoverable margin sits. Pass-through here should be high, often near 100 percent of landed-cost change, but it should be implemented as a structured policy: round to charm prices, respect promotional cadence, batch into weekly or bi-weekly waves so the shelf does not look chaotic. The discipline is to do it consistently across thousands of SKUs without manually touching each one. This is the part of the catalog where most of the operational complexity lives.

The third tier is the discretionary tail — long-tail SKUs, niche brands, gift items, seasonal. Here the elasticity is low, the consumer is not comparing across retailers, and the appropriate pass-through is often greater than the supplier increase. The retailers we talk to who recover margin most successfully through a tariff cycle do it by quietly resetting price ladders on the tail, not by chasing percentage points on the headline items. The trade-off is that this is exactly the part of the catalog where governance is hardest. Without a clear policy, the tail becomes a graveyard of one-off decisions that no one can explain six months later.

What the data says about who is actually paying

It is worth being precise about where the cost has actually landed so far, because the answer is uneven and recent enough that intuition is not a reliable guide.

The Cavallo, Llamas and Vazquez paper estimates retail pass-through to date at roughly 20 percent — that is, of the cost increase at the border, about a fifth is currently visible at the shelf. State Street and others, using different methods, put the consumer's share of the total tariff burden after seven months at up to 43 percent. The remaining 57 percent is being split between upstream manufacturers, importers, and wholesalers. That share is not stable. The Dallas Fed expects further drift toward the consumer as inventory rolls and as contract reopeners arrive.

The unevenness inside that average is the operational story. Cheaper varieties of consumer goods rose roughly 5 percent over the year ending September 2025 — about double the rate of premium varieties. Households at the bottom of the income distribution face the steepest effective inflation from this dynamic. For a mid-market retailer with a meaningful trade-down customer, this matters: holding the line on entry-tier private label and value-tier national brands is both a margin question and a customer-retention question, and the two answers do not always agree.

The other shift worth naming is in private label. US private-label sales reached roughly $330 billion with share above 23 percent, and the mid-market private-label tier has grown 65 percent since 2021. That gives mid-market retailers a real lever — a private-label SKU at the right quality and price point can hold a customer who would otherwise trade away from a tariff-exposed national brand. But it only works if the private-label price ladder is managed alongside the national brand response, not as a separate workstream.

The pricing architecture this requires

What does the operating model look like once you accept that pass-through is a portfolio of decisions, not a single number?

Three things have to be true.

Cost signals have to flow through the pricing engine, not around it. Most pricing teams still receive supplier cost notices as PDFs that route through procurement, then merchandising, then pricing — by which time the cost is two weeks old. The retailers that hold margin push landed-cost change directly into the pricing system as a first-class input, with the SKU-level tariff line broken out. That lets the system compute pass-through proposals automatically, by tier, against the policy each tier has set.

Competitive monitoring has to be continuous on the reference set, not the whole catalog. A common mistake is to scrape every competitor for every SKU and drown in noise. The reference set — the 500 to 2,000 items where the consumer or a key competitor genuinely sets the ceiling — needs near-real-time competitor pricing. The other 28,000 SKUs do not. Concentrating the monitoring budget on the right set is what makes the tier-one rule operable.

The pricing review has to be weekly, in writing, with exceptions queued. A quarterly committee cannot keep pace with the cost notice cadence. The cadence that works is a weekly review of the cost-change queue, a fast policy-based approval on the items that match a pre-defined rule, and a separate exceptions queue — the items where the policy does not give a clean answer and a category manager has to make a judgement. Exceptions should be a few percent of decisions, not the default. If the exception queue is bigger than the auto-approved queue, the policy is wrong, not the queue.

This is the architecture our team has been building toward across pilots in CEE retailers through 2025 and 2026, and it is the architecture you can see explained in plainer terms on the Retailgrid product overview. The point is not the tool. The point is that the operating model only works if the cost signal, the competitive signal, and the policy logic live in the same place and update on the same cadence.

What this doesn't change

It is worth being explicit about what tariff pass-through is not a moment for.

It is not a moment to abandon competitive discipline on key value items. The consumer is more sensitive to KVI moves, not less, in a high-inflation environment. Retailers who quietly raise prices on the items shoppers compare across retailers will lose traffic faster than they recover margin.

It is not a moment to overhaul promotional architecture. Most promotional ROI problems are structural and exist independently of the tariff cycle. Fixing promotions during a tariff response usually means fixing neither.

It is not a moment to delay private-label investment. If anything, the tariff cycle accelerates the case for private label — particularly mid-market tier private label, where the consumer is trading down from premium national brands. The retailers who emerge from the cycle with structurally higher private-label share will hold gross margin that retailers chasing headline price increases will not.

And it is not a moment to make the response invisible. Customers can read your shelf. They know prices are moving. A clear, simple story — held on the basics, moving on the items where everyone is moving, investing in private label — outperforms a quiet across-the-board increase that the consumer detects on their own.

A 90-day pricing review focused on tariff exposure

For a C-suite that wants to move from posture to plan, a 90-day exercise is usually enough to get the operating model into shape. The shape we recommend is roughly this.

In the first thirty days, build the tariff-exposure map. For every SKU, attach a tariff-content estimate (the share of landed cost subject to current tariff schedules) and a tier classification (reference, middle, tail). This is a one-time data exercise; the output is durable. The map is the artefact the CFO and CCO should both be reading from.

In the second thirty days, codify the tier policies. Write down — literally, in a one-page document per tier — what the pass-through rule is, what the competitive reference is, who approves exceptions, and what the recovery path looks like. Run the prior month's price changes against the new policy and see how many decisions it would have approved cleanly. If the answer is below 80 percent, the policy is too vague.

In the third thirty days, operationalise the weekly review. Move from quarterly to weekly cadence. Build the cost-change queue. Assign one analyst to own it. Measure two things: the share of decisions auto-approved by policy, and realised margin movement against forecast. If those two numbers move together over the quarter, the architecture is working.

This is unglamorous work. No platform announcement at the end, no AI keynote, no transformation press release. What there is, done well, is a hundred or two hundred basis points of operating margin that competitors are giving up because they treated pass-through as one decision instead of a thousand small ones. In 2026, that is the difference between hitting the quarter and missing it.

The tariff wave is not going to recede on a clean schedule. The pricing organisation built for continuous response will outperform the one built for the next discrete event. Build the portfolio. Run it weekly. Tell the consumer a story they can read.